When Insurance Costs Outrun Inflation, Safety Becomes the Lever

Feeling Better About Inflation

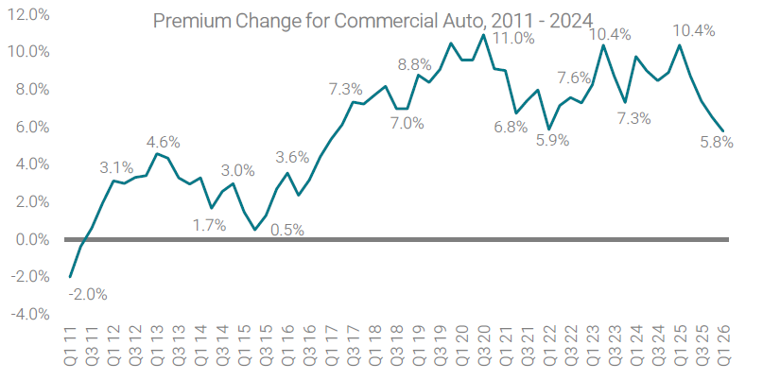

Inflation has been a buzzing topic of late. No one likes paying more for goods, services, parts, labor, or fuel, but if you want to do something that makes an inflation rate of “only” 4% feel more manageable, take a look at commercial auto insurance premium increases.

In May 2026, the American Transportation Research Institute (ATRI) published, Trucking’s Rising Insurance Costs: Issues and Opportunities. The report reinforces the magnitude of the commercial auto insurance crisis that continues to plague the American economy.

While the ATRI report focuses on trucking, the issues they raise span the entirety of the Commercial Auto spectrum. Using data from the Council of Insurance Agents and Brokers, ATRI details the fact that average annual premium increases have continued to outpace inflation by a factor of more than 2x for the better part of the last decade.

Source: Council of Insurance Agents & Brokers, Q1 2026 P&C Market Survey

Another cheery fact from the ATRI report is that smaller fleets (which also account for a disproportionate share of the nation’s transportation network), have been hit hardest. ATRI notes that “Fleets with 5 to 25 trucks spent 20.3 cents/mile on liability insurance premium costs in 2024…twice as much as fleets with 101 to 250 trucks at 10.4 cents/mile.”

Despite these premium increases, insurance companies continue to lose significant amounts of money in the commercial auto line of business, posting combined ratios north of 100 for over a decade.

Clearly, this is not a sustainable state of affairs.

When insurance costs are rising faster than inflation, safety is not just a compliance priority. It is one of the few levers fleets can still pull.

This post could focus on the need for tort reform and other mechanisms to counter a litigation environment running amok. While true reform would undoubtedly help, given the range of jurisdictions at play, meaningful change will take time. So, what could have a more immediate impact?

Putting aside circumstances involving outright fraud, by definition, litigation requires an incident in which one party was harmed by another. So, no accident = no litigation.

Research from organizations such as Swiss Re also shows that injury severity plays a major role in trial outcomes. That means there is value not only in reducing the number of crashes, but also in reducing the severity of the crashes that do occur.

As we have detailed in past posts, reducing speeding through a well-managed telematics and driver coaching program has a rapid, significant, and documented impact on:

- Reducing the frequency of accidents.

- Minimizing the severity of those accidents that still happen.

So, if you have not yet leaned into driver coaching and want to buck the trend of premium increases, there is no better time to start than now.

As you contemplate this, there is another nugget from the ATRI report that may help to motivate you. ATRI’s research shows that companies that retain more of their own risk realize significantly lower cost of risk. Specifically, for those retaining 5% or less, their cost of risk (premium plus retained liability losses) ran between 12 and 15 cents per mile. In contrast, the corresponding cost of risk for those retaining more than 5% and up to 30%, was 8 cents per mile.

While eating your own cooking may prompt a bit of anxiety, it also creates a powerful incentive to actively manage risk rather than simply absorb another year of premium increase. Based upon ATRI’s data, it also looks like it’s worth it.

The fleets that treat telematics as a compliance tool will just keep collecting data. The fleets that turn that data into coaching, accountability, and safer behavior will be in a much better position to control their costs of risk. When insurance costs are rising faster than inflation, safety is not just a compliance priority. It is one of the few levers fleets can still pull.